China Updates

Accounting and Taxation

- On 28 October 2024, the General Administration of Customs of the People's Republic of China issued the "Measures for the Administration of Customs Duties on Import and Export Goods."

These Measures will come into effect on 1 December 2024. These measures will govern the collection and administration of import and export tariffs as well as customs-collected taxes on imports, introducing significant procedural updates for enterprises.

Keyhighlights of the New Measures:

The Measures comprise eight chapters and eighty-four articles, covering a wide range of customs tax administration aspects, including general provisions, calculation of duties, special circumstances for duty collection, confirmation of duty amounts, refund, supplementary collection, and recovery of duties, duty guarantees, and tax enforcement.

Enforcement Actions

-

Issuing written notices to banking financial institutions to transfer deposits or remittances equivalent to the amount of duties owed by the taxpayer

-

Seizing or detaining goods or other properties of the taxpayer or withholding agent with a value equivalent to the amount of duties owed.

Integration with the ‘Customs Tariff Law’

The revised "Measures for the Administration of Customs Duties on Import and Export Goods" summarise the achievements of past customs tax administration reforms and clarify new approaches for future customs tax administration. As a departmental regulation accompanying the "Customs Tariff Law," these measures will directly impact the daily declaration activities of enterprises and customs’ supervision functions. Particularly, the newly established procedure for "confirmation of duty amounts" should be given special attention.

Changes to Enterprise Declaration and Tax Payment Procedures

Starting 1 December 2024, the process for enterprise declaration and tax payment, as well as customs review and confirmation, will undergo changes.

- Past: Enterprises declare all tax-related elements —— Customs reviews all tax-related elements —— Enterprises pays taxes —— Customs conducts subsequent supervision

- After the New Law Takes Effect: Enterprises declare tax-related elements and tax amounts —— Enterprises pay taxes —— Customs confirms tax amounts (within three years after the enterprise pays taxes or after the release of goods)

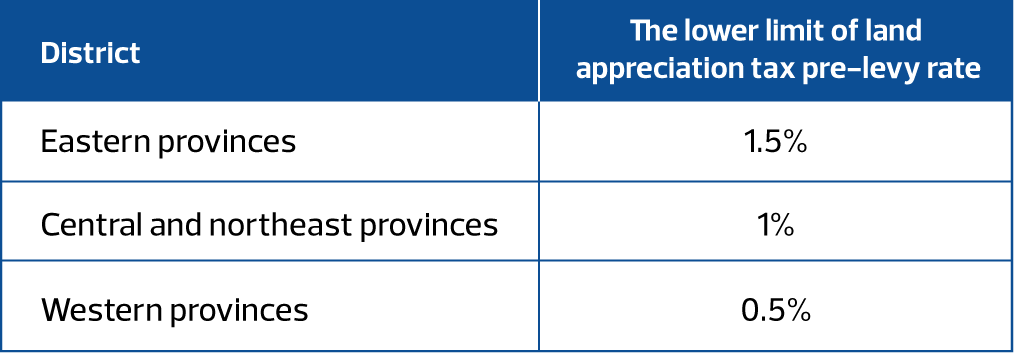

- Announcement of the State Taxation Administration on Reducing the Lower Limit for the Pre-Levy Rate of Land Appreciation Tax

On 13 November 2024, the State Taxation Administration issued an announcement to adjust the lower Limit for the Pre-Levy Rate of Land Appreciation Tax (LAT), effective from 1 December 2024. The adjustments aim to enhance the regulatory role of LAT.

The key points of the announcement are as follows:

- According to the relevant provisions of the PRC LAT, the lower limit for the pre-levy rate of LAT has been reduced by 0.5%.

- After the adjustment, excluding affordable housing, the lower limit of the pre-levy rate for each region and province is outlined in the table below: